SPACs: Navigating the Hype and Reality

Understanding SPACs

In 2021, Special Purpose Acquisition Companies, or SPACs, dominated the public markets, capturing the attention of investors, startups, and regulators alike. However, the frenzy around SPACs is now facing a reckoning, as concerns about transparency and market performance have come to the forefront.

A SPAC, short for Special Purpose Acquisition Company, is essentially a public shell company with the sole purpose of acquiring a private company and taking it public. Often referred to as a "blank check" company, SPACs go public before they've identified a specific acquisition target. This unique approach has been around for decades, but it gained immense popularity in recent years. Notably, high-profile companies like WeWork, Grab, and SoFi chose to debut via SPAC in 2021, reflecting the growing interest in this alternative to the traditional IPO.

Why SPACs Are Attractive

There are several reasons why both investors and startups are turning to SPACs. For startups, it offers a faster and less volatile path to going public compared to the traditional IPO. Additionally, investors see SPACs as an opportunity for high-reward investments with limited risk.

One remarkable aspect of SPACs is their accessibility. Almost anyone can initiate a SPAC, and this has attracted a diverse group of individuals and entities. Prominent figures such as entrepreneur and venture capitalist Peter Thiel, former quarterback Colin Kaepernick, and baseball executive Billy Beane have all ventured into the SPAC arena. Chamath Palihapitiya, known as the "SPAC King," has launched multiple SPACs, starting with Virgin Galactic in 2019. This accessibility, however, has led to criticism that SPACs offer a "shortcut" to the traditional IPO, bypassing many of the stringent regulatory requirements. Electric vehicle startups, in particular, have been quick to embrace SPACs, generating substantial buzz even before producing vehicles for sale.

Challenges and Criticisms

One contentious issue surrounding SPACs is the practice of making forward-looking statements about the financial performance of the target company after a SPAC has identified it. Unlike traditional IPOs, SPAC mergers often involve optimistic growth projections that some critics argue can mislead investors. In response to these concerns, the Securities and Exchange Commission (SEC) proposed new rules in March 2022 to curb these practices and provide greater protections for investors.

Despite the initial excitement surrounding SPACs, their market performance has lagged. The performance of an exchange-traded fund (ETF) that tracks SPACs dropped by 37% over the past year, as of late March, while the S&P 500 grew by nearly 18% during the same period.

The SPAC Process: A Closer Look

To better understand SPACs, let's break down the process:

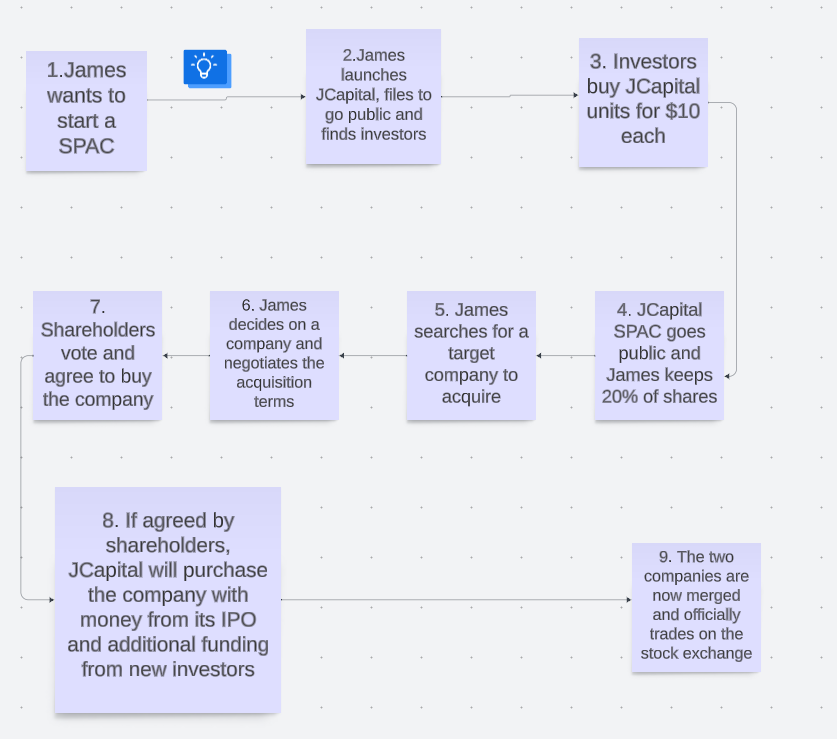

- Formation and Public Offering: A sponsor or a team with significant business experience forms the SPAC. It creates a holding company with no operational business and conducts a roadshow to attract interested investors. These investors purchase units, which typically cost $10 each and include one share of the company and a warrant to buy more shares in the future. The funds raised during the initial public offering (IPO) go into a blind trust and cannot be accessed until shareholders approve an acquisition transaction or redeem their shares. The SPAC then goes public and trades on an exchange like any other publicly traded company.

- Target Identification and Acquisition: Once the SPAC is public, the sponsors search for a target company to acquire. There are generally no restrictions on the type of company a SPAC can acquire. The sponsors typically have two years to identify and announce an acquisition. If they fail to do so within this timeframe, the SPAC dissolves, and shareholders receive their money back.

- De-SPAC Process: After agreeing on the terms of the acquisition, the sponsors propose the target to shareholders. Unlike an IPO, the de-SPAC acquisition is not considered a public offering, allowing for forward-looking statements in filings. Shareholders have the opportunity to vote on the acquisition and can redeem their shares if they disagree with the sponsor's choice. Following approval and the completion of redemptions, the acquisition can proceed.

- Additional Capital Raise: The initial SPAC raise typically covers only a portion of the purchase price. To bridge the gap, sponsors can seek additional capital through a Private Investment in Public Equity (PIPE) transaction. Once the final capital is secured, the target company can go public.

- Regulatory Approval: The target company must gain approval from regulators. While the SPAC itself is already public and has been approved by the SEC, the target company must meet the same regulatory requirements as in a traditional IPO. Once approved, the ticker symbol changes to reflect the acquired company's name, and it begins trading as a typical public company.

Benefits and Concerns

SPACs offer unique advantages. They allow retail investors to participate in public offerings with redemption options, should the SPAC fail to find a target company within the specified time. The SPAC merger process is typically faster and more negotiable than a traditional IPO, offering greater certainty to shareholders and employees. Institutional investors are also attracted to SPACs due to the potential for high-reward investments with limited risk. For sponsors, the potential for significant financial gain makes SPACs a compelling opportunity.

However, the current structure of SPACs has faced criticism for the significant financial incentives it provides to sponsors. Sponsors typically pay a nominal amount to acquire 20% of the SPAC shares, even if the acquired company underperforms. This has led to calls for reform to align sponsor interests more closely with those of shareholders.

SPACs in the UK

Turning our attention to the United Kingdom, launching US-style SPACs in London faced certain challenges due to the UK listing regime. However, the UK Government recognized the international interest in SPACs and ordered a review of the listing process. As a result, the Financial Conduct Authority (FCA) introduced rule changes in 2021 that make the UK market more accommodating to SPAC listings. These rule changes include safeguards like redemption options, ring-fencing of funds raised from public shareholders, and shareholder approval requirements for proposed business combinations.

These changes bring the London market more in line with other jurisdictions in terms of SPAC deal structures. The extent to which US-style SPACs will feature more prominently in London remains to be seen and will depend on market dynamics. However, these rule changes represent a significant development in making SPACs part of the UK equity landscape.

The Future of SPACs

SPACs have emerged as an alternative to the traditional IPO, offering unique opportunities and challenges. While they provide accessibility and flexibility for startups and investors, they have also faced criticisms for potential investor misguidance and sponsor incentives. As regulatory changes are considered, the future of SPACs remains uncertain, and their impact on the IPO landscape will continue to evolve. Investors, startups, and regulators will need to carefully navigate this evolving landscape to ensure transparency and investor protection in the SPAC market.

In conclusion, SPACs have undoubtedly disrupted the traditional IPO landscape, offering new opportunities and challenges. As they continue to evolve and adapt, we can expect ongoing debates over their structure and regulation. The SPAC phenomenon has reshaped the way companies go public and has provided a platform for startups to access public markets more rapidly. However, it's essential to strike a balance between accessibility and investor protection to ensure the long-term sustainability of SPACs in the financial world. The coming years will reveal whether SPACs can maintain their appeal and navigate the regulatory changes necessary for their maturation in the global marketplace.